![]()

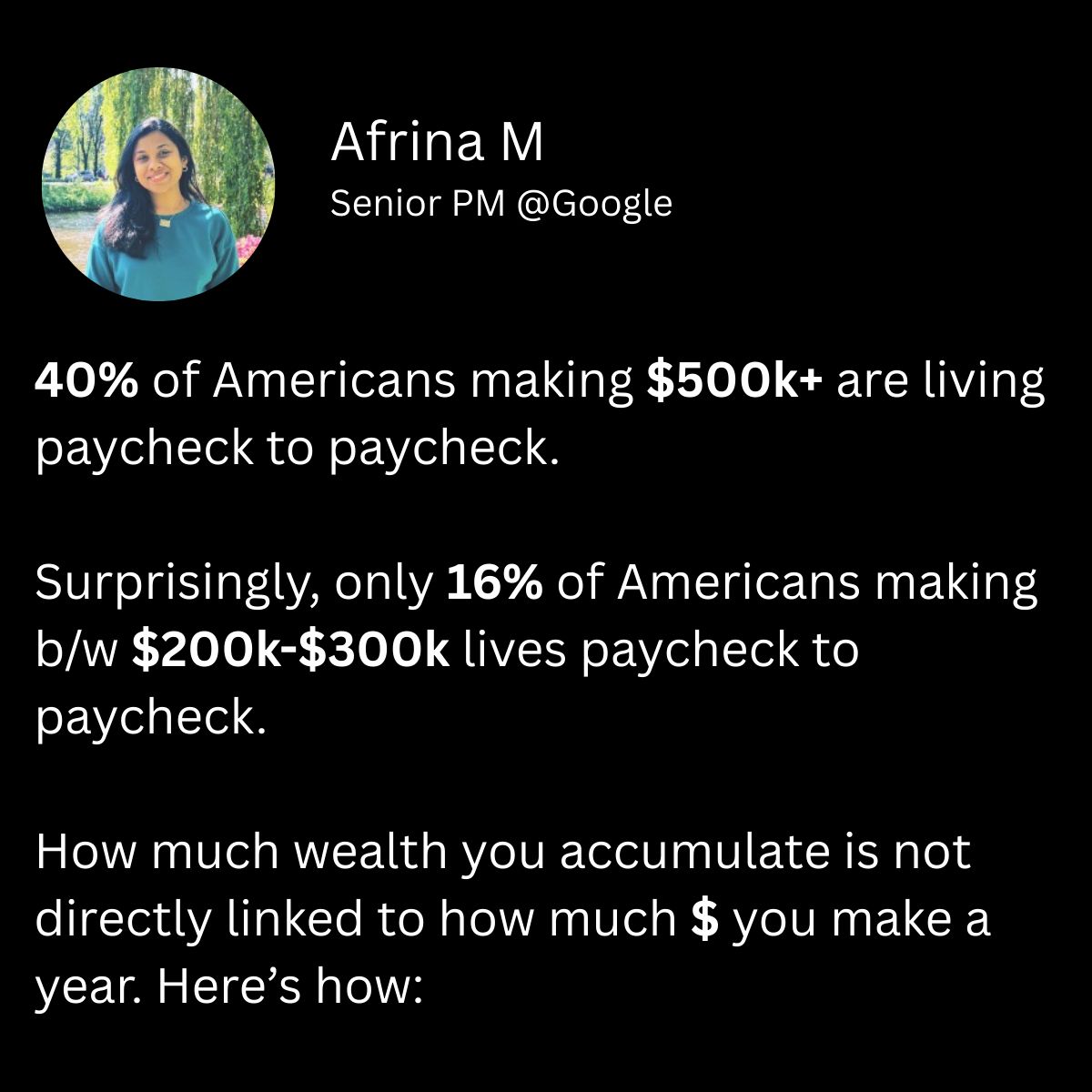

When $500,000 Isn’t Enough: The Quiet Math Behind High-Income Pressure

Submitted by Hilpan Moxie Wealth Management, LLC. on March 20th, 2026

I want to walk you through a real scenario.

Not a hypothetical.

Not a headline.

A real household.

(Prompted by a sharp observation from Afrina M. on high-income pressure— this is what the math looks like inside a real household.)

A family of four.

Two kids.

They earn about $500,000 per year, composed of base salary, RSU equity compensation and bonus income.

By almost any measure, that should feel like more than enough.

And yet, if we slow the conversation down and map it out carefully, it doesn’t.

The Starting Point: What $500K Actually Becomes

Let’s begin with what actually hits their life.

After federal and state taxes, payroll taxes, maxing their 401(k), running a Mega Backdoor Roth, funding healthcare and dependent care FSAs, and correcting for RSU under-withholding-

What’s left is roughly:

~$20,000 to $22,000 per month

That’s the real number.

Not what they earn.

Not what shows up on paper.

What actually funds their life. (This range reflects meaningful variation by state, someone in Texas keeps more than someone in California or New York. The math still works the same way.)

The Life They’ve Built (Reasonable, Not Excessive)

Now let’s layer in how they live.

|

Category |

Monthly |

|

Housing (rent or mortgage equivalent) |

~$5,000 |

|

Private school (2 kids) |

~$4,500 |

|

Travel |

~$2,300 |

|

|Discretionary |

~$4,000 |

|

Groceries, insurance, utilities, activities |

~$4,000 |

|

Sub Total |

~$19,800 |

On paper, that leaves about $200–$2,200 per month of margin.

That’s not lavish.

That’s not reckless.

That’s a household doing things intentionally and still operating with almost no room for error.

Now Add What Should Be Happening

Because here’s the part that rarely gets discussed.

If this household is doing things right, they’re not done.

529 Plans

Using annual (2026) gift exclusions, currently $19,000 per child, two kids means $36,000 per year.

That’s $3,000/month.

After-Tax Investing

Even after maxing retirement accounts, the math demands more:

∙ Conservative: 10% of income = $50,000/year = $4,200/month

∙ Better: 20% = $100,000/year = $8,300/month

The New Reality

Being conservative, 529s plus 10% after-tax investing adds:

+$7,200/month

Updated monthly need: ~$27,000

Monthly net income: ~$20,500

Result: A deficit of -$6,500/month

Let That Sit for a Second

This is a $500,000 household.

Doing things responsibly. Intentionally. Without extravagance.

And they are running a structural deficit.

Now Layer in the Dream

The home.

A $2.5M home in a good school district, this price point exists in Boston, Seattle, Denver, Northern Virginia, and the Bay Area alike.

Mortgage, taxes, insurance, maintenance: ~$14,700/month

Replacing $5,000 rent: +$9,700/month increase

New monthly need: ~$36,700

Monthly net income: ~$20,500

Final position: Deficit of -$16,200/month

“But My Income Will Grow”

Maybe. Probably, even.

But here’s what growth actually buys you:

∙ At 6–7% annual growth → ~$28K/month net in five years → still behind

∙ At 10% annual growth → ~$33K/month net in five years → barely catching up

And that assumes no lifestyle creep, no income disruption, no market correction in your equity comp.

Growth is real. It’s just not the escape hatch it feels like.

So What’s Actually Going On?

Nothing is “wrong.”

This isn’t overspending.

This is structure.

The system is fully allocated, before you’ve done anything irresponsible.

The Real Tradeoffs

At this level, life becomes a series of explicit decisions:

∙ Private school vs. public school

∙ Homeownership vs. liquidity

∙ Lifestyle today vs. margin tomorrow

∙ Growth assumptions vs. current reality

You can have almost all of it.

But not all of it at once, not without making future income do work it hasn’t earned yet.

The Trap

The trap isn’t low income.

The trap is this:

High income creates the feeling of flexibility, without actually delivering it.

The money is real. The constraints are just as real.

Most people at this level never sit down and map it out. They feel vaguely uneasy, successful on paper, pressured in practice- and they can’t explain why.

This is why.

The Only Question That Matters

Do you want to maximize lifestyle today, or build margin for tomorrow?

There’s no universally correct answer.

But there is a consequence to each, and most people are making that choice by default rather than by design.

$500,000 is a great income.

It provides access, options, and real opportunity.

But it does not eliminate tradeoffs.

And if you never slow down to make those tradeoffs explicit, you don’t feel wealthy.

You feel tight.

That feeling isn’t a character flaw. It’s math.

If you’re navigating equity compensation, concentrated stock positions, or simply trying to make all the pieces fit together, the most valuable thing isn’t more information. It’s clarity on the full picture.

That’s the work worth doing.

If this feels familiar, this is usually where the questions start:

How much should I actually be saving at this level?

How do RSUs affect my real income?

Am I too concentrated in my company stock?

Start here: